What is the 4% rule for ETF? — A clear guide

This article explains what the rule means, how it translates to ETF only portfolios, what historical evidence and modern critiques say, and practical steps you can take to model a sustainable withdrawal plan. Use these steps as a starting framework and adapt assumptions to your personal situation.

What the 4% rule means and where it comes from

The 4% rule says you withdraw 4% of your portfolio in the first year of retirement and then raise that same dollar amount each year for inflation. William Bengen introduced this guideline after testing historical U.S. market sequences, framing it as a planning baseline rather than a promise of safety; his method used past market data to show when a fixed, inflation adjusted withdrawal held up over long retirements William Bengen paper.

That approach gave people a simple way to think about a safe withdrawal rate and it influenced later work, including the Trinity research that expanded tests across different stock and bond mixes. The phrase safe withdrawal rate grew around these studies because they looked at real historical sequences to see how often a fixed initial withdrawal would last over a 30 year period.

Keep in mind that the original formulation is a rule of thumb. It is useful as a starting point for planning, but it does not guarantee results for every investor or time period. Different allocations, fees, taxes, and the particular retirement start date change the math materially.

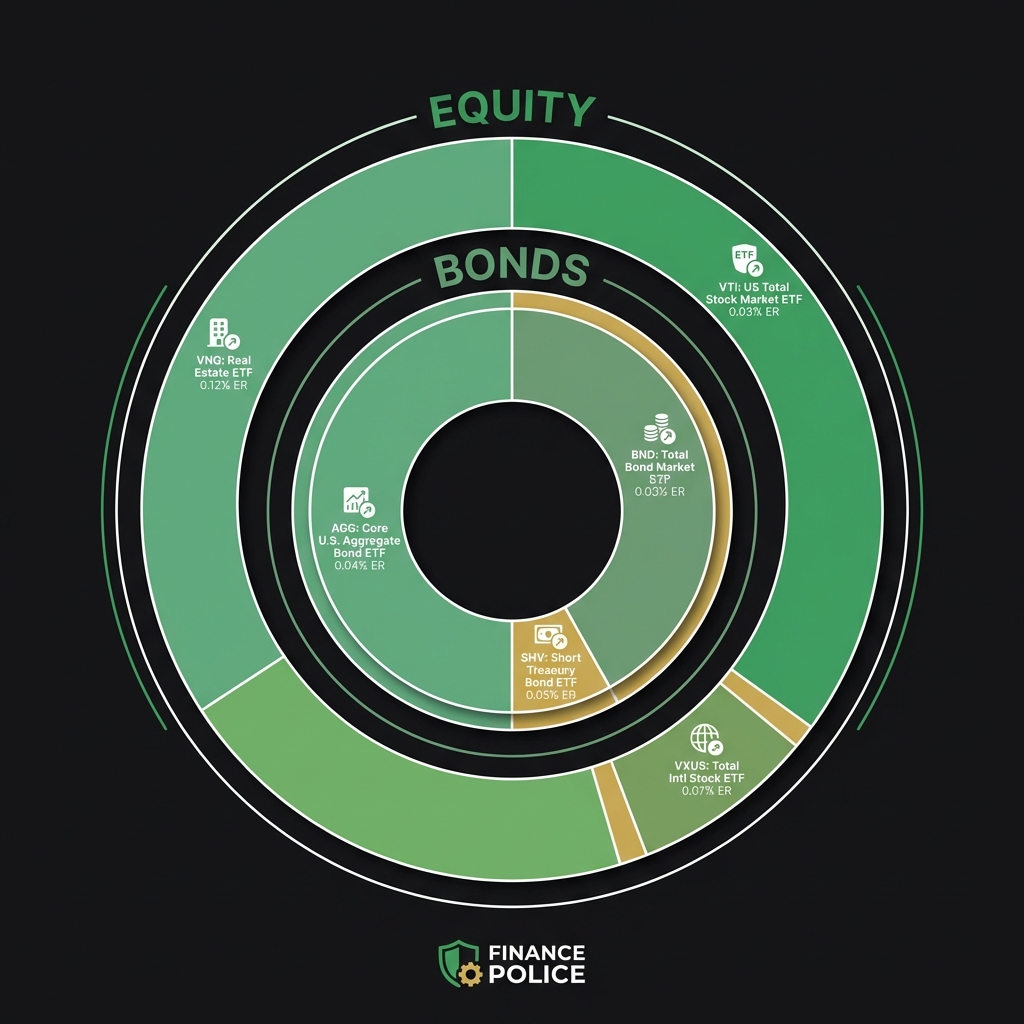

How the 4% rule applies to ETF portfolios

Mechanics for ETF-only portfolios, and how to start an etf

The arithmetic behind the 4% rule is the same whether your holdings are ETFs, mutual funds, or individual securities. You still calculate 4% of the portfolio value, take that dollar amount in year one, and then adjust that dollar amount for inflation in each subsequent year. Conceptually this makes the rule portable to ETF-only portfolios, but practical effects change the net amount you can spend.

For ETF investors, expense ratios, trading costs, and how you take withdrawals matter. Expense ratios reduce net returns over time, which lowers the sustainable withdrawal level compared with a theoretical model that assumes zero or minimal fees. Trading and bid ask costs can be small per trade but add up if you trade frequently to fund annual cash needs.

Tax treatment also changes the picture. Withdrawals from taxable accounts, tax deferred accounts, and Roth style accounts are handled differently by tax rules. That affects how much of a withdrawal is available to spend after taxes, and it can influence whether a nominal 4% withdrawal meets your real spending needs.

When you plan an ETF retirement withdrawal strategy, list the expense ratios and likely tax treatment for each holding. Model those costs into your withdrawal plan rather than assuming a raw 4% will be fully spendable.

What historical evidence says about success and limits

Historical simulation work from William Bengen and follow-up studies like the Trinity analysis showed that a 4% initial withdrawal often worked well across many U.S. 30 year periods when portfolios included a meaningful equity allocation. Those foundational tests used past market returns to report how frequently a fixed initial withdrawal would survive a three decade retirement, giving planners an empirical baseline to start from Trinity Study report (see the Safe Withdrawal Rate Series Early Retirement Now).

However, the historical results vary by the retirement start date and by portfolio allocation. Periods that began with weak returns or high inflation made a fixed 4% withdrawal more likely to exhaust a portfolio in a thirty year window. Treat the historical success rates as contextual evidence, not a guarantee.

Treat 4% as a baseline starting withdrawal. Model expense ratios, trading costs, taxes, rebalancing, and sequence of returns scenarios. Set operational rules for withdrawals and triggers to switch to an adaptive method if needed.

Also remember that history uses realized past returns. Future returns, fee environments, or tax rules can differ. That means a cautious planner treats the 4% rule as a sensible starting assumption and then layers modeling, buffers, and rules for adjustment to fit personal circumstances.

Sequence of returns risk and modern critiques

Sequence of returns risk is the idea that the timing of gains and losses matters when you are withdrawing money. Two retirements with the same average returns can have very different outcomes if one has bad returns early and the other has bad returns late. This concept explains why identical average returns can produce different survival outcomes for fixed withdrawal plans Sequence of returns risk overview (see Kitces for a detailed analysis Kitces and Schwab’s primer Schwab).

Practitioner and academic work through 2024 and beyond highlights that SORR is a primary driver of failures for a strict inflation adjusted 4% rule, especially when markets start retirement with steep declines. Lower expected future returns make the rule more fragile because there is less upside to offset early losses.

a simple scenario tester for early retirement return sequences

–

USD

Use varying early year returns to see sequence effects

Because of sequence risk, many modern researchers and planning practitioners recommend adaptive strategies or guardrails. Those approaches adjust withdrawals or pause inflation adjustments after bad early returns, lowering the chance of running out of money compared with a strict fixed rule.

Dynamic and guardrail alternatives to a fixed 4%

Several adaptive withdrawal strategies are commonly discussed. One approach is a spending band or guardrail where withdrawals rise or fall within a band tied to portfolio performance. Another is a percentage-of-portfolio rule, where each year you withdraw a fixed percentage of current portfolio value rather than a fixed inflation adjusted dollar amount. A third is a hybrid rule that uses a target inflation adjusted payment but adjusts that payment up or down if portfolio value moves beyond certain thresholds. Research suggests these methods can lower failure risk compared with a strict 4% inflation adjusted withdrawal Morningstar research.

The tradeoff is clear. Adaptive methods tend to reduce the chance of portfolio exhaustion, but they also create more variability in year to year income. That can be a real planning cost for people who need steady monthly cash to meet fixed living expenses. The decision comes down to how much income stability you value versus how much longevity risk you are willing to accept.

To choose among options, compare hypothetical income paths under each method for your assumed returns, fees, and tax profile. If you prioritize predictable income, you might accept a higher failure probability or seek outside income solutions like partial guaranteed income. If you prioritize reducing the chance of running out of money, a guardrail or percentage based approach will often look more attractive.

How to implement a 4%-based plan with ETFs step by step

Step 1, pick a starting withdrawal rate. Use 4% as a baseline, then adjust that starting figure if your time horizon, allocation, fees, or tax situation suggest a different number. Think of 4% as an initial assumption to test, not a fixed prescription.

Step 2, build a simple model that includes expected expense ratios, likely taxes on withdrawals, and a rebalancing plan. Rebalancing cadence matters because selling gains to fund spending or to return to target allocation affects future return paths. Include conservative cost assumptions when you test sustainability Vanguard guidance on withdrawal strategies.

Step 3, set operational rules. Decide how you will take cash from your ETF holdings, which accounts you will draw from first for tax efficiency, and how often you will rebalance. Document triggers for switching to an adaptive rule if early returns are poor. For example you might plan to pause inflation adjustments or switch to a percentage of portfolio withdrawal if the value drops below a pre set threshold.

Test your ETF withdrawal assumptions

Run your numbers with conservative fee and tax assumptions, and save your checklist so you can review it annually as conditions change.

Save checklist

Step 4, pick low cost ETFs and a rebalancing cadence. Low expense ratios reduce the drag on returns, which helps the sustainable withdrawal level. Annual or semi annual rebalancing is common for many investors and keeps allocation risk in check without excessive trading.

These steps create a replicable workflow for ETF retirement withdrawal strategy. The goal is not to lock into a number forever but to create a defensible starting plan and clear triggers for adjustments when reality diverges from assumptions.

Common mistakes, pitfalls, and questions to ask before you withdraw

Avoid these frequent errors. First, do not treat historical success as a guarantee of future results. Second, do not ignore fees and taxes when modeling withdrawals. Third, do not let a single year of poor returns force emotional decisions without consulting your rules or model. Many failures are avoidable when people plan and document their approach ahead of time Investor.gov retirement income basics.

Decision checklist before you commit to a withdrawal rate. Confirm your time horizon and spending needs. Estimate likely taxes given which accounts you will draw from. List the expense ratios of your ETFs and choose a rebalancing cadence. Decide on a contingency plan for sequence shocks, such as reducing withdrawals or drawing from a short term cash buffer.

Also consider whether you have access to guaranteed income sources, like a pension or annuity, that can cover core living costs. Having a portion of guaranteed income can make a withdrawal plan less sensitive to sequence of returns risk and reduce pressure to spend from the portfolio in bad years.

Scenario A: A diversified ETF portfolio with a moderate equity allocation is often the reference case in the 4% literature. Conceptually, a 4% starting withdrawal gives a simple cash number to plan around, and historical tests show it succeeded in many U.S. thirty year sequences when equity exposure was meaningful. Use that scenario to test whether fees and taxes change the sustainable level after you add realistic costs into your model William Bengen paper.

Scenario B: A conservative portfolio with a higher bond allocation will generally have lower expected long run returns and so a fixed 4% withdrawal is less resilient in principle. Historical simulations that vary stock bond mixes show differing success rates, which is why your allocation choice matters when you set a starting withdrawal amount Vanguard guidance on withdrawal strategies.

The Final checklist. Model assumptions explicitly, including expected returns, expense ratios, and taxes. Check your ETF expense ratios and trading costs. Decide on a rebalancing cadence and write down withdrawal mechanics. Set decision triggers for switching to an adaptive rule, like a guardrail or percentage of portfolio rule. Verify your sources and revisit the plan annually.

Applied thoughtfully, the 4% rule is a useful planning baseline for ETF investors. It is not a guarantee, but it gives a simple starting point to model and compare alternatives, including dynamic rules that can reduce failure risk in difficult return sequences.

The 4% rule asks you to withdraw 4% of your portfolio in year one and then increase that dollar amount each year by inflation to maintain purchasing power.

Yes, the rule applies conceptually to ETF portfolios, but you should model expense ratios, trading costs, and taxes since they affect net sustainable withdrawals.

Many planners treat 4% as a starting point. Consider adaptive guardrails or percentage of portfolio rules if you want lower failure risk in bad early return sequences.

If your assumptions or comfort with variability change, consider a guardrail or percentage based approach. Revisit your plan regularly and update it when tax rules, fees, or your personal situation change.

References

- https://www.retailinvestor.org/pdf/Bengen1.pdf

- https://www.trinity.edu/rjensen/343wp/TrinityStudy1998.pdf

- https://earlyretirementnow.com/safe-withdrawal-rate-series/

- https://www.retirementresearcher.com/sequence-of-returns-risk-safe-withdrawal-rates-2024

- https://www.kitces.com/blog/understanding-sequence-of-return-risk-safe-withdrawal-rates-bear-market-crashes-and-bad-decades/

- https://www.schwab.com/learn/story/timing-matters-understanding-sequence-returns-risk

- https://www.morningstar.com/articles/2025/is-the-4-percent-rule-still-viable

- https://investor.vanguard.com/retirement/withdrawal-strategies/4-percent-rule

- https://financepolice.com/advertise/

- https://www.investor.gov/financial-advice/retirement/retirement-income

- https://financepolice.com/advanced-etf-trading-strategies/

- https://financepolice.com/category/investing/

- https://financepolice.com/

You May Also Like

How to earn from cloud mining: IeByte’s upgraded auto-cloud mining platform unlocks genuine passive earnings

USDC Treasury mints 250 million new USDC on Solana