As cryptocurrencies become increasingly integrated into the traditional financial system, major digital assets are evolving beyond investment vehicles into important tools for payment and settlement. In response, regulators worldwide are establishing regulatory frameworks to support innovation and payment efficiency while mitigating risks related to money laundering, terrorist financing, and other illicit activities.

As critical infrastructure for fund flows and trading, cryptocurrency exchanges must continuously enhance their compliance and risk management capabilities. Leading platforms adhere to globally recognized AML and sanctions standards, ensuring consistent risk control practices across source-of-funds verification, transaction monitoring, and regulatory reporting where required.

For cryptocurrency exchanges, the most influential standard-setter for risk control standards is the Financial Action Task Force (FATF), the international body that develops AML and counter-terrorist financing frameworks. More than 200 jurisdictions worldwide have committed to incorporating FATF recommendations into local regulations.

Since 2019, FATF has formally classified cryptocurrency exchanges as Virtual Asset Service Providers (VASPs). By 2025, FATF-aligned jurisdictions cover the majority of major crypto markets, meaning that most global liquidity now operates within a unified compliance framework. Exchanges that fail to align with these standards risk gradual exclusion from mainstream markets, liquidity, and institutional partnerships.

To operate legally, exchanges must implement FATF-compliant controls, including customer due diligence, transaction monitoring, sanctions screening, and standardized reporting mechanisms. Non-compliance may result in significant penalties, license revocation, or delisting.

Know Your Customer (KYC) requires users to verify their identity using valid documentation. It is a core AML measure derived from FATF standards, designed to deter illicit activity and provide traceable identity records, thereby reducing the entry of fraudulent or illegal funds.

Regulatory frameworks globally mandate KYC for crypto exchanges. In the EU, AMLD5 classifies exchanges as obligated entities, while the Transfer of Funds Regulation (TFR) requires sender and recipient identification for cross-border crypto transfers. In the United States, exchanges have been subject to bank-level AML requirements since 2013.

For users, effective KYC lowers the risk of account misuse, isolates illicit funds, and helps protect compliant assets from enforcement actions or indirect exposure to illegal financial activity.

Transaction monitoring is not only a core component of an exchange's risk control framework, but also a mandatory legal obligation under global regulatory regimes. Its primary purpose is to ensure that platforms are not exploited for illicit financial activities.

Under FATF global standards, cryptocurrency exchanges, as Virtual Asset Service Providers (VASPs), are required to uphold monitoring obligations equivalent to those of traditional financial institutions, including real-time screening of counterparties and fund flows. The EU's TFR regulation and AMLD framework go further by requiring VASPs to implement effective monitoring procedures. In particular, the TFR emphasizes interactions with self-hosted addresses, mandating the collection of sender and recipient information. For transfers exceeding EUR 1,000, exchanges must also verify that the address is owned or controlled by the customer.

To meet these requirements, exchanges implement a combined off-chain and on-chain monitoring and tracing framework. Off-chain monitoring focuses on account behavior, enabling real-time detection of activities such as high-frequency wash trading, abnormal large deposits or withdrawals, and coordinated manipulation across multiple accounts. On-chain tracing leverages specialized blockchain analytics tools to analyze and cluster transaction paths, reducing compliance risks arising from anonymity. This process enables exchanges to trace asset origins and identify whether funds are linked to darknet activity, hacking incidents, or sanctioned entities. For regulatory high-risk areas, such as privacy tokens, mixing services, and other anonymization techniques, the system automatically elevates risk levels and triggers appropriate risk controls or manual reviews.

Robust transaction monitoring not only ensures compliant and stable platform operations, but also helps isolate illicit funds and abnormal trading behavior. By reducing the distortion caused by fake volume and illicit activity, it supports genuine liquidity, effective price discovery, and a fair and healthy trading environment.

Within the global AML/CFT (anti–money laundering and counter–terrorist financing) framework, asset freezing is a fundamental compliance obligation.

FATF standards explicitly require financial institutions to implement appropriate risk mitigation measures once money laundering or terrorist financing risks are identified. In particular, when a customer or transaction matches a sanctions list, VASPs are legally required to freeze assets and block transactions “without delay.” In 2025 alone, U.S. enforcement actions for AML/CFT violations resulted in fines exceeding USD 1.1 billion, with cryptocurrency exchanges accounting for USD 927.5 million of that total. Major cases involved platforms such as OKX, BitMEX, and KuCoin, with core violations stemming from inadequate AML and KYC implementation.

FATF guidance further emphasizes that VASPs and related parties must possess the technical capabilities to enforce sanctions and risk mitigation measures, including the ability to restrict or freeze assets where appropriate, in order to effectively implement targeted financial sanctions and disrupt criminal networks.

Accordingly, when risk control systems detect high-risk indicators or sanctions matches, the activation of restrictions or asset freezes has become industry standard. These actions are not discretionary platform decisions, but legally mandated requirements under a globally harmonized framework. Failure to comply may expose platforms to substantial fines or even more severe regulatory consequences.

The Suspicious Activity Report (SAR) mechanism is a statutory requirement under global AML/CFT frameworks. Under FATF standards, financial institutions, including banks, payment providers, and cryptocurrency exchanges, must confidentially report suspected money laundering, terrorist financing, or criminal activity to the national Financial Intelligence Unit (FIU) within required timeframes. Triggers may include unexplained large transfers, unclear sources of funds, or interactions with high-risk addresses.

A standard SAR workflow typically begins with the detection of suspicious activity, followed by an internal investigation that includes evidence collection and enhanced due diligence. Where necessary, accounts or transactions may be restricted or frozen, with complete records preserved for compliance purposes, and the platform cooperating with the relevant Financial Intelligence Unit (FIU) or judicial authorities.

This process is governed by two core principles. Timeliness requires that SARs be filed within prescribed timeframes, generally within 30 days in the United States (extendable to 60 days in complex cases), or without undue delay in the European Union. Confidentiality strictly prohibits platforms from disclosing monitoring activities or SAR filings to customers, with violations subject to legal penalties.

Beyond combating financial crime, the SAR mechanism serves to contain risk and protect compliant users. In most cases, once users provide reasonable explanations or supporting documentation, accounts can be restored following the completion of compliance reviews.

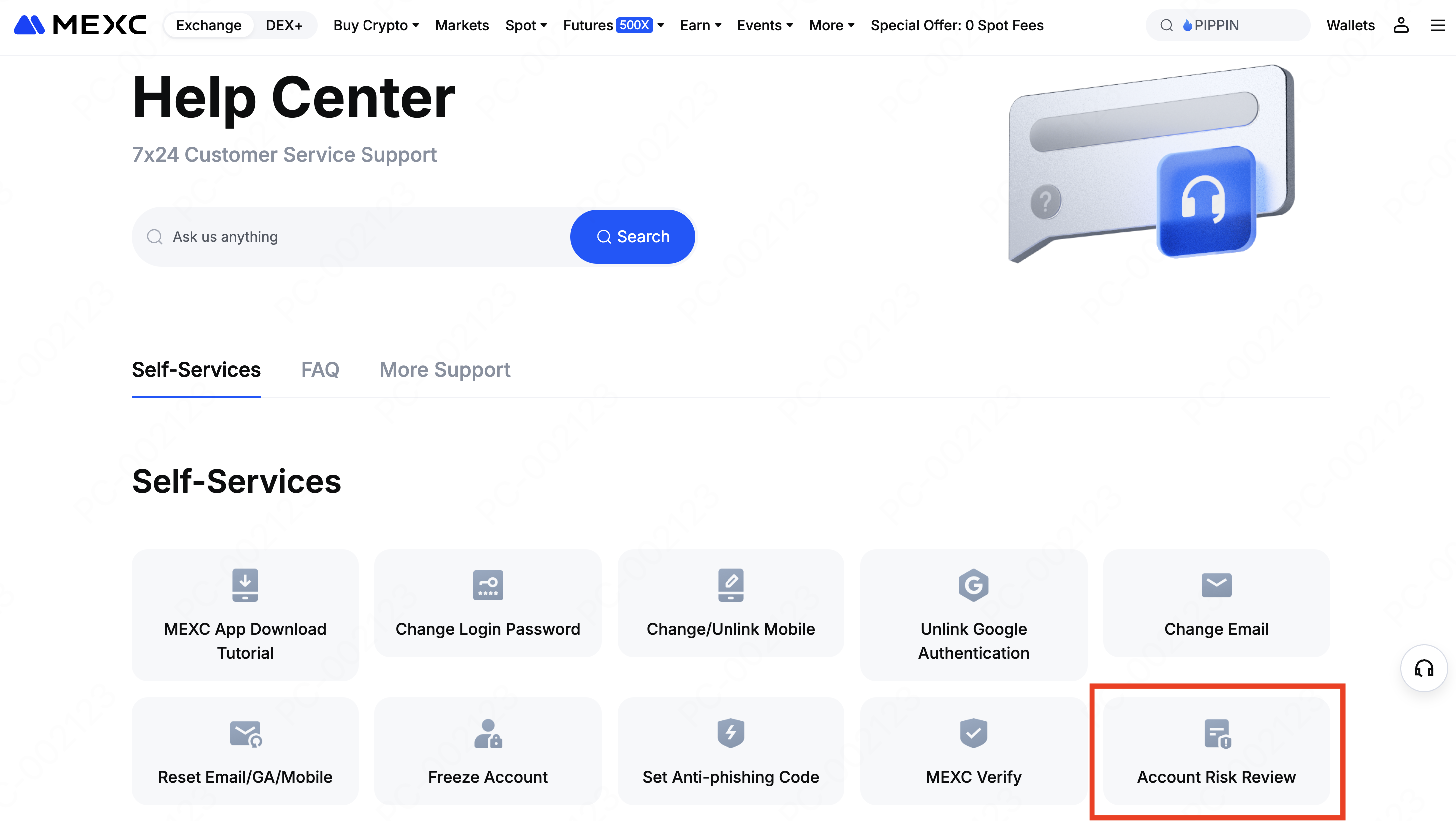

When risk indicators prompt further review, users may be asked to submit additional information. If restrictions are applied, MEXC provides a clear and accessible appeals process.

Users can access the submission page via Official Website → Help Center → Account Risk Review, where identity and source-of-funds documents can be uploaded. Reviews typically involve document verification (around three business days) followed by risk behavior analysis. Progress can be tracked on the page, with updates provided by email.

Meanwhile, MEXC has recently implemented a series of optimizations to its risk control user experience, with the goal of establishing a more transparent, efficient, and user-centric appeals mechanism. A dedicated appeals task force has been set up to accelerate the processing of account unfreezing requests. Affected users can submit appeals through officially designated channels, with customer service leads coordinating follow-ups promptly. This mechanism significantly improves the accessibility of user feedback, enabling more direct and efficient communication.

To safeguard overall platform security and comply with applicable regulatory requirements, compliance and risk control remain non-negotiable foundations. While enforcing strict risk control measures, the platform simultaneously provides supporting verification and appeals procedures to ensure that all decisions are handled with appropriate diligence and fairness.

MEXC's risk control appeals framework continues to evolve based on community and user feedback. The platform is committed to offering clearer guidance, smoother communication channels, and sufficient, practical avenues for users to exercise their right to appeal within a well-defined institutional framework.

As cryptocurrencies become increasingly integrated into the traditional financial system, regulatory frameworks and standards continue to mature, guiding the industry toward healthier and more sustainable development. These efforts aim to balance innovation and convenience for users and investors while effectively curbing illicit activities.

As a key infrastructure layer driving the adoption and application of digital assets, exchanges must proactively adapt to this trend. Striking a balance between upholding compliance standards, blocking illegal activity, and minimizing disruption to legitimate user trading and experience has become a central challenge, and a critical long-term priority, for exchanges.

MEXC's next-generation risk control framework systematically integrates these compliance benchmarks into daily platform operations, covering core areas such as identity verification, source-of-funds checks, suspicious transaction monitoring, and multi-account manipulation detection. This ensures that all risk assessments are traceable, evidence-based, and auditable.

Ultimately, the objective of risk control is not to restrict legitimate trading activity, but to focus on identifying and preventing risk, deterring malicious behavior, and protecting the vast majority of rule-abiding users. A healthy and sustainable market cannot exist without rules. Only with clear standards and robust safeguards can traders compete fairly and platforms achieve long-term, stable growth.