What Banks Use XRP? Complete List of Financial Institutions Using Ripple

- First, understand what XRP is and how it works.

- SBI Holdings, Santander, and PNC Bank lead institutional XRP adoption across Asia, Europe, and North America.

- Over 300 financial institutions use RippleNet infrastructure, though not all implement XRP directly for liquidity.

- XRP enables cross-border settlements in 3-5 seconds with fees averaging $0.0002 per transaction.

- On-Demand Liquidity (ODL) eliminates pre-funded currency accounts, freeing up trapped capital for banks.

- Ripple's SEC case concluded in 2025, providing regulatory clarity for XRP's use in banking operations.

- Regional leaders in Latin America, Middle East, and Asia demonstrate strongest XRP implementation for remittance corridors.

What Banks Use XRP Today? Leading Institutions by Region

- SBI Holdings / SBI Remit (Japan) - Full ODL implementation

- Axis Bank (India) - Active since 2017

- Kotak Mahindra Bank (India) - RippleNet member

- UnionBank (Philippines) - ODL for remittances

- ChinaBank (Philippines) - XRP-backed transfers

- Siam Commercial Bank (Thailand) - Real-time settlements

- Woori Bank (South Korea) - RippleNet for payments

- Shinhan Bank (South Korea) - RippleNet for payments

- Commonwealth Bank of Australia - Exploring Ripple technology

- Vietcombank (Vietnam) - Exploring solutions

- PNC Financial Services (USA) - First major U.S. bank

- Canadian Imperial Bank of Commerce (CIBC) - ODL adoption

- American Express (USA) - B2B payments

- Cross River Bank (USA) - Cross-border payments partner

- Frankenmuth Credit Union (USA) - Offers XRP services

- Santander (Spain/UK) - One Pay FX service

- Standard Chartered (UK) - Asia-Middle East corridors

- MUFG Bank (Japan) - RippleNet member

- Zand Bank (UAE) - Launched 2025

- Al Ansari Exchange (UAE) - Cross-border payments

- National Bank of Fujairah (UAE) - Cross-border solutions partner

- RAKBANK (UAE) - UAE-India corridor

- Qatar National Bank (Qatar) - Philippines corridor

- Riyadh Bank (Saudi Arabia) - Remittance systems

- Travelex Bank (Brazil) - First Latin American ODL

- Banco Rendimento (Brazil) - Remittance flows

- Interbank (Peru) - ODL customer

- Standard Bank (South Africa) - RippleNet integration

- MoneyGram (Global) - Historic partnership

- BeeTech (Brazil) - Cross-border fintech

- InstaReM (Singapore) - Regional transfers

- SendFriend (USA) - International payments

- Remitr (Global) - Payment provider

1. Major Banks Using XRP Ripple Technology

2. North American Banks Adopting XRP Infrastructure

3. Asian Financial Institutions Leading XRP Adoption

4. Latin American and Middle Eastern Banking Partners

- See all XRP applications and use cases.

How Banks Use XRP Technology for Cross-Border Payments?

The Traditional Banking Problem XRP Solves

How XRP Acts as a Bridge Currency

- Will XRP replace SWIFT entirely? Explore the full comparison here.

RippleNet vs XRP: Understanding the Difference

Why Banks Are Going to Use XRP Over SWIFT Systems

Frequently Asked Questions

Conclusion

- Learn more about XRP technology in our comprehensive guide.

Related Articles:

Popular Articles

What Is a MEXC Futures Guaranteed Stop-Loss Order?

1. What is a MEXC Futures guaranteed stop-loss order?A Futures guaranteed stop-loss order is a professional paid risk management feature designed to address extreme volatility in the cryptocurrency ma

How to Buy Crypto with Credit/Debit Card: MEXC Step-by-Step Guide

Key TakeawaysMEXC accepts credit and debit cards from Visa and MasterCard networks across 38 supported countries with transparent 2% processing fees.You can buy crypto with credit card on MEXC after c

Buy Crypto with Bank Transfer: Complete SEPA Payment Guide for Europe

Key TakeawaysBuy crypto with SEPA transfers for faster processing times (2 hours with SEPA Instant) and lower fees than traditional payment methods.SEPA crypto purchases are available in 30 European c

Hot Crypto Updates

View More

Ripple (XRP) 7-day Price Change

The Latest Ripple (XRP) price has shown significant movement over the past week. In this article, we'll examine its current XRP price, 7-day performance, and the market factors shaping XRP's trend,

Ripple (XRP) Price Prediction: Market Forecast and Analysis

Understanding the price prediction of Ripple (XRP) gives traders and investors a forward-looking perspective on potential market trends. XRP price predictions aren't guarantees, but they provide

Trending News

View More

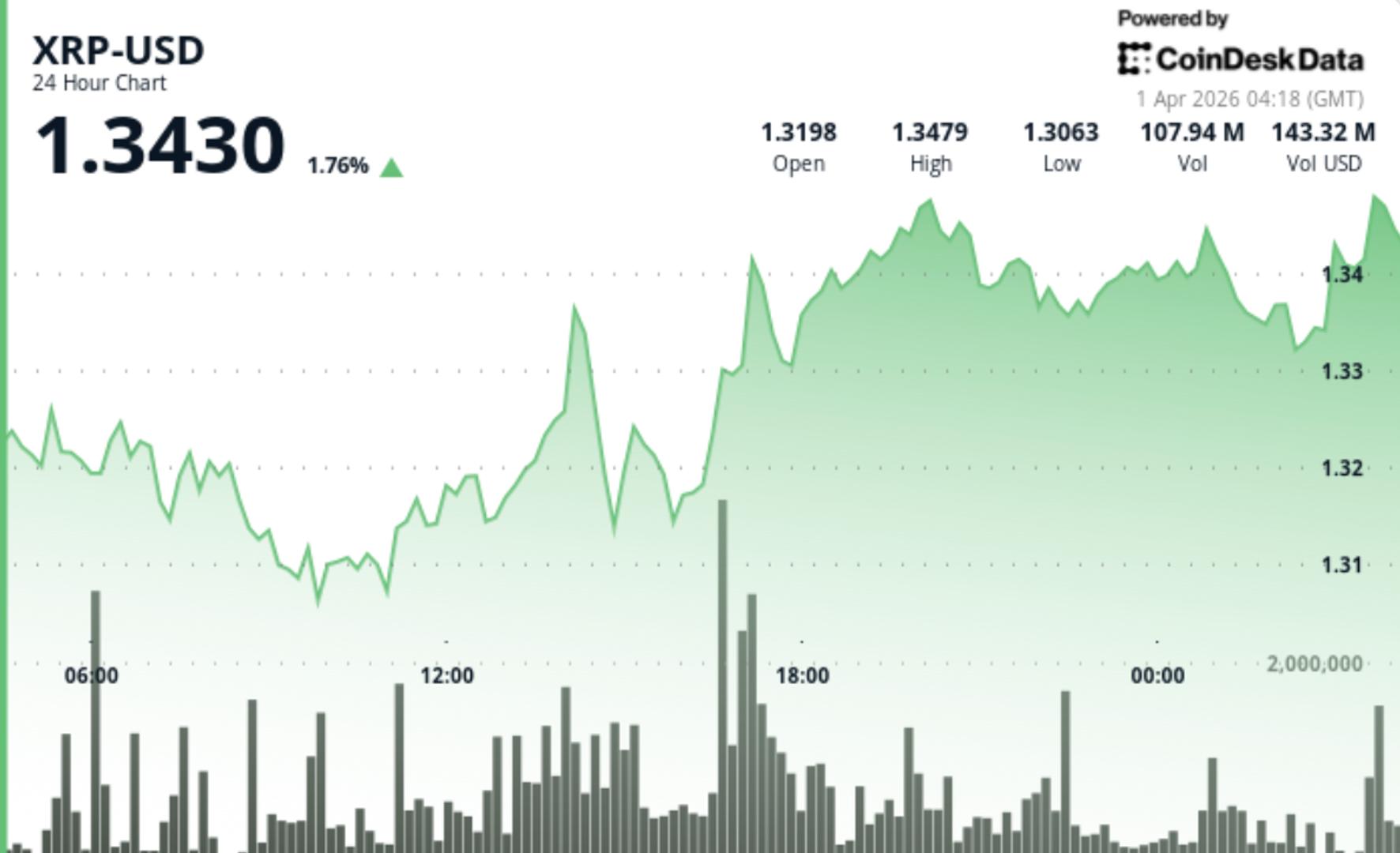

XRP holds $1.34 as supply tightens but price fails to break higher

XRP is seeing large amounts of tokens leave exchanges, reducing available supply — but price isn’t responding yet. The token is hovering near $1.34 after a

XRP Is Quietly Leaving Binance. A Hidden Signal Says Something Is Building Beneath It

XRP is struggling to hold $1.35. The market is preparing for further downside. And beneath the price action, a quietly growing group of investors appears to have

Related Articles

What Is a MEXC Futures Guaranteed Stop-Loss Order?

1. What is a MEXC Futures guaranteed stop-loss order?A Futures guaranteed stop-loss order is a professional paid risk management feature designed to address extreme volatility in the cryptocurrency ma

How to Buy Crypto with Credit/Debit Card: MEXC Step-by-Step Guide

Key TakeawaysMEXC accepts credit and debit cards from Visa and MasterCard networks across 38 supported countries with transparent 2% processing fees.You can buy crypto with credit card on MEXC after c

Buy Crypto with Bank Transfer: Complete SEPA Payment Guide for Europe

Key TakeawaysBuy crypto with SEPA transfers for faster processing times (2 hours with SEPA Instant) and lower fees than traditional payment methods.SEPA crypto purchases are available in 30 European c